SThree is the world’s number one recruitment firm focused solely on science, technology, engineering and maths-related roles (typically abbreviated to STEM).

I think it's a high-quality dividend growth stock and I added it to the UK Dividend Stocks Portfolio and my personal portfolio back in April 2020.

However, after only 19 months I have decided to sell SThree, so in this post, I want to explain why. More specifically: why I thought SThree was suitable for a dividend growth portfolio, why I bought it in early 2020 and why I sold it at the start of November.

Table of Contents

- Exceptional but unsustainable share price gains

- Consistently high returns on capital

- Relatively consistent growth for a cyclical business

- Deep expertise in STEM recruitment

- A consistent strategy over many years

- Some benefits from network effects

- Some benefits from switching costs

- Operating in secular growth markets

- Why I bought SThree in the middle of a crash

- SThree's valuation is now far less attractive

Exceptional but unsustainable share price gains

This chart from ShareScope/SharePad shows how SThree's share price increased by around 150% since it joined the portfolio 19 months ago.

This rapid price increase was, of course, driven mostly by the general recovery of stock markets globally after the initial crash in early 2020.

I'm sure many other stocks have produced even more impressive gains since April 2020, but in my portfolio, SThree generated the best post-crash returns.

- Website: sthree.com

- Purchase price: £2.15 on 08/04/2020

- Sale price: £5.84 on 05/11/2021

- Holding period: 1 year 7 months

- Total return: 146%

- Annualised total return: 87% per year

These results are far better than I would normally expect, so it's important to stay grounded and to realise that a 150% gain in a year and a half is just not normal.

In this case, it was due to the combination of a market crash (which usually only happens once every decade or so) and an unprecedented amount of government support that has (so far) stopped the economy from crashing along with the market.

These two factors mean that investors who were brave enough to put money into the market during the crash have made unusually high short-term returns.

In summary, my investment in SThree worked out very well, which is mildly interesting. What is much more interesting is why I bought the company in the first place.

In other words, why do I think SThree is a high-quality dividend growth stock? Here are some of the main reasons:

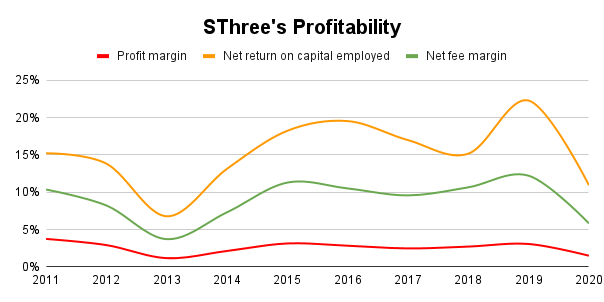

Consistently high returns on capital

As part of my five-step investment strategy, one of the first things I look for is a track record of consistently high returns on capital employed.

Of course, SThree is a recruitment business and recruitment is cyclical, so its results over the years have been somewhat bumpy rather than fantastically smooth and consistent. However, overall I would say that SThree has produced consistently high returns.

For example, SThree's return on capital was above 10% in every year but one over the last decade, averaging 16% over the period. That's far better than most companies.

As for its return on sales (profit margin), it has been consistently below 5%, which is very low. That’s a potential concern, but in this case, it’s caused by an accounting quirk.

The accounting quirk is that many contractors (also known as temps or freelancers) who find their next project through SThree have their wages paid through SThree as well. Those wages show up as revenues, but they’re passed straight to the contractor so those wage “revenues” effectively have a profit margin of zero, and that skews the overall profit margin downward.

If we strip out contractor wages and just look at recruitment fees, then SThree’s return on recruitment fees (known as "net fee margin") jumps up to a more acceptable average of 9%.

Relatively consistent growth for a cyclical business

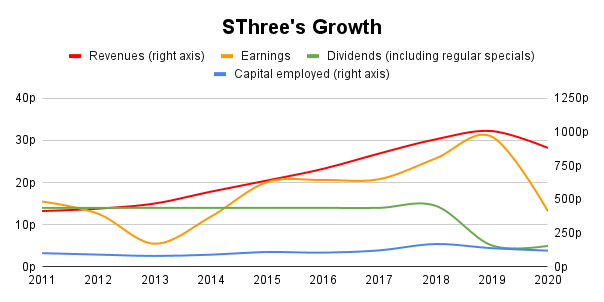

SThree’s consistently high return on capital has given it lots of profit to reinvest for growth over many years.

For example, the company started out as a two-man operation in 1986 and by 2005 it was generating revenues of more than £300 million. Revenues peaked at just over £630 million before the crash of 2009 and peaked again at just over £1300 million before the pandemic.

So SThree has produced lots of growth, and that growth has been mostly funded by low-risk retained earnings rather than higher-risk debt.

The chart above shows SThree’s impressive growth over the last ten years, but it’s important to remember that this is a cyclical business. The period shown in the chart covers the low point of one cycle (shortly after the 2009 crash) to the peak of another (just before the pandemic), so the growth in that chart is short-term and unsustainable.

If you look further back into SThree's history it becomes clear that it has repeatedly grown from one cycle to the next, and that’s about the most you can expect from a cyclical business.

Some people will say that you shouldn't invest in cyclical stocks if you're after consistent dividend growth, but I disagree. I think more defensive stocks should make up the bulk of a dividend portfolio, but I don't see anything wrong with having a reasonable amount invested in high-quality cyclicals as long as they're purchased at attractive valuations.

Deep expertise in STEM recruitment

High-quality companies are usually masters of their trade, which is how they're able to generate high profits for decades even in the face of very stiff competition. And to become a master of your trade, you need to develop a niche set of skills over decades.

This is exactly what SThree has done. It started out as an IT recruitment firm more than 30 years ago and, over decades, has carefully expanded into the largely similar areas of science, engineering and maths/finance.

To avoid the risk of becoming an unfocused jack of all trades, SThree serves each branch of STEM through a separate brand:

- Real (life sciences)

- Computer Futures (technology),

- Progressive (engineering)

- Huxley (math/finance)

Computer Futures was the company’s original identity, so this brand has been around since 1986. Progressive was launched in 1990, Huxley in 1995 and Real in 1998. So all of SThree’s four core businesses have been in operation for more than 20 years.

SThree has tightened its focus even further over the last decade, by moving from the traditional fairly even split between permanent candidates and contractors, to being more than 75% focused on contractors.

The story behind this shift is a classic case of investing in your biggest opportunities.

Having crunched the numbers a few years ago, SThree's management realised that contractors had a 40% higher average lifetime value and a consistently higher return on capital than permanent candidates. On top of that, the market for contractors was growing faster than the market for permanent staff.

It was a no-brainer, so over the last decade SThree has significantly shifted its focus to contractors and the result is net fees from contractors roughly doubling from 2011 to 2019.

A consistent strategy over many years

Another common feature among quality companies is that they stick to the same basic strategy for years and often decades. Of course, the details change, but the basics remain the same.

In SThree's case, its strategy for many years has revolved around a few simple ideas:

Focus on highly skilled niche candidates: SThree is a specialist recruiter so it’s focused on value over volume. In other words, instead of trying to place a zillion candidates who are relatively easy to find on job boards like Monster (e.g. junior Python programmers), it’s focused on placing harder to find experts who have very specific skills and experiences so they can be dropped into a project and add value from day one. These experts also tend to be highly paid, which means more commission for SThree.

Focus on STEM: SThree is strategically focused on STEM because it’s full of niche disciplines that require highly skilled people who are often hard to find. STEM is also growing faster than the overall recruitment market, it has roles that tend to be highly paid and there’s more demand for talent than supply, all of which makes STEM an attractive recruitment market.

Focus on being the market leader in the best STEM markets: Different STEM markets have different strengths and weaknesses, so SThree is focused on those that have a reasonably large and robust economy, significant science, technology, engineering or finance sectors, global connections, high wages, more demand for STEM talent than supply and preferably weak competitors.

One of the first countries to meet these criteria was Germany, where SThree opened an office in 2002 and is now a leading STEM specialist. The Netherlands was another early international office and SThree has grown to become the leading STEM specialist in that country.

Market leadership is a good strategic goal because recruitment firms can have network effects, and market-leading network effects can be a powerful and durable competitive advantage.

Some benefits from network effects

Network effects exist in platform businesses like Rightmove or AutoTrader, which bring together buyers and sellers in specific markets such as housing or secondhand cars. The platform with the most sellers attracts the most buyers and vice versa, so network effects often produce market leaders that are borderline monopolies.

This concept also applies to recruitment because it’s a market where skill is sold by candidates and bought by companies. That’s why we have very large online recruitment platforms like LinkedIn, Monster and Indeed.

Similarly, SThree’s main websites are set up like platforms to attract clients and candidates. But SThree isn’t a hands-off platform looking to connect buyers and sellers with as little friction as possible. Instead, it's a more hands-on business that needs detailed knowledge of and trusted relationships with clients and candidates, so it isn't quite the same as high volume recruitment platforms like Monster or Indeed.

Even so, SThree does have platform-like features, especially in its fast-growing "employed contractor" business.

Employed contractors are directly employed by SThree, and one of the main reasons they choose to be employed by SThree is that SThree typically has relationships with more companies that are looking for STEM talent than the competition, and that means a wider selection of projects for contractors to choose from. The same attraction exists for companies. When they have a project that needs expert contractors as soon as possible, it’s easier to get them from SThree as it typically has more STEM contractors on its books than the competition.

However, although I do think SThree benefits from network effects, it isn't the clear market leader in all its key markets, so I don't think SThree's network effects are anywhere near as strong as those of dominant platforms like Facebook, Amazon or Rightmove.

Some benefits ffrom switching costs

Switching costs exist when it takes customers a significant amount of time and/or effort to switch to a competitor.

For SThree, this mostly occurs in its employed contractor business. Contractors who are directly employed by SThree are much more likely to look for their next contract through SThree because it already has all their details, it already knows what contracts they're looking for and it knows when the contractor's current contract is due to end.

Of course, the cost of switching to another recruitment firm isn't insurmountable, but it's definitely easier to stick with the same recruitment firm as long as it can supply attractive projects at the right time.

This makes employed contractors somewhat "sticky". These switching costs are a useful feature and they help SThree grow by increasing the lifetime value of each contractor and reducing contractor churn, but they're not a silver bullet.

If you want to see real switching costs, have a look at how many companies stick with the same IT systems for decades because they know it will take months and possibly years of disruptive work to switch from one HR system or one insurance underwriting system to another.

Operating in secular growth markets

One of the defining features of SThree is that it sits at the crossroads of two long-term secular growth trends.

The first long-term trend is the increasing demand for STEM roles across the world. This is being driven by several factors:

-

Longevity: Advances in medical technologies are rapidly increasing our ability to extend life, leading to an expected 120% growth in life science roles over the next ten years

-

Technological proliferation: Computers are now an essential part of work and life for billions of people and this trend is expected to continue, leading to an expected doubling of technology roles over the next ten years

-

Energy transition: The shift to a low and eventually net-zero carbon economy is increasing demand for engineers today and that demand is also expected to double over the next ten years

The second long-term trend is the shift to flexible working, with more and more companies and candidates preferring to have greater flexibility, working and hiring on a project-by-project basis with fewer opting for permanent employment.

So the demand for STEM professionals is expected to continue growing, but there has also been a decrease in the number of potential STEM candidates because more people have retired in recent decades than have been born.

This is creating a structural mismatch between the demand for and the supply of experienced STEM professionals. That, in turn, makes experienced STEM professionals harder to find and more expensive to hire, which is the ideal situation for a specialist STEM recruitment firm like SThree.

To summarise everything so far, I would say that SThree is a focused business that has repeatedly proven its ability to move into new STEM markets and new countries, consistently leveraging its expertise, scale and exposure to high-growth markets to generate above-average returns over several decades. In other words, I think SThree is a quality business.

But identifying a high-quality dividend stock is only the first step in my five-step investment strategy.

The second step is to estimate their fair value and the third step is to buy them when there's a significant margin of safety between the current price and that fair value estimate. And that's why I bought SThree in the middle of a stock market crash.

Why I bought SThree in the middle of a crash

In March 2020, COVID-19 cases were skyrocketing and the UK was entering the first of several national lockdowns. It was a very memorable time for reasons both good and bad.

From an investment point of view, almost all the news was bad and the FTSE 100 simply fell off a cliff, going from 7,403 on February 21st to 4,994 by March 23rd.

If you're mostly invested in high-quality companies then the most important thing you can do at times like these is to avoid panic-selling.

If you own quality companies then it's unlikely that their intrinsic values will have fallen as much as their share prices. So instead of selling, a more rational course of action (if you're interested in generating decent investment returns) is to go bargain hunting.

So that's what I did.

I looked at my stock screen and one of the top stocks (ranked 14 out of 200 or so) was SThree.

The stock screen told me that SThree had grown by an average of 6% per year over the previous decade, had average returns on capital of 16%, it didn't have a lot of debt and it required almost no investment in expensive property or equipment (capex) to grow.

And yet, this company had a dividend yield of almost 7%. Or at least it did, because the day before I invested in SThree the dividend was suspended.

Now, you may think I'm an idiot, because what sort of dividend investor invests in a company that isn't paying a dividend? And yes, perhaps I am an idiot. But I'm also a realist and I know that no dividend is safe. In fact, the pursuit of ultra-safe dividends above all else can lead to below-average returns because you end up investing in National Grid and not much else.

So rather than investing only in companies that are virtually guaranteed to pay dividends, I'm comfortable casting my net a little wider and can accept that dividend cuts and suspensions are a fact of life. I try to limit them of course, but I don't have unrealistic expectations.

So SThree's dividend was suspended, but I didn't think it would be suspended for very long. In the April 2020 issue of The UK Dividend Stocks Newsletter I said this:

The pandemic is likely to have a very significant impact on the global economy in 2020 and perhaps 2021, so it would be madness not to expect this to have a short-term impact on companies like SThree. My base assumption is that recruitment will take a massive hit in 2020, but SThree has several important features which should make it one of the more resilient recruitment firms out there:

Almost no borrowings: As a capital-light business, SThree has borrowings of less than £5m compared to 2019 profits of more than £40m. It does have £64m of lease liabilities, but this is only three times its ten-year average earnings, so overall I would say the balance sheet is strong.

Variable expenses: SThree’s cost base is mostly recruitment consultant commissions, which are based on revenues. If revenues go down (which I’m sure they will in the short-term), then commissions go down too. Historically this has cushioned profits to the point where the company still made a profit and maintained its dividend through the financial crisis.

Industrial diversity: SThree has almost 10,000 clients who operate in just about every sector of the economy. The company doesn’t provide much information on this, but I assume it has many clients operating in relatively defensive sectors including food retailers, drug companies and makers of toilet roll or soap.

Tech focus: Technology recruitment is at the heart of SThree. Most programmers can work from home, so while retail stores are closed, I suspect many tech departments in companies like Next* or Burberry are working pretty much as they were before the crisis. In addition, pure tech companies make up about 20% of SThree’s revenues, and many of these will be relatively unharmed by the virus.

Contractor focus: SThree is heavily weighted towards contractors rather than permanent roles (75% vs 25% of gross profits) and the contractor market tends to be more resilient during downturns.

Obviously, the current situation is unprecedented for a modern economy, so we don’t really have a clue about what’s going to happen. That is the reality of it. However, in my opinion, SThree is probably more durable than the vast majority of companies [and] my assumption is that full lockdown is unlikely to last long enough to kill off a robust company like SThree.

Fundamentally then, my assumption was that SThree could return to its pre-pandemic dividends within a handful of years, and at that point, it would have a dividend yield of almost 7% at the then-current share price of £2.15.

If that happened then I would either get a very handsome dividend, or the share price would appreciate, giving me a very handsome capital gain. Either way, SThree looked like a good investment in early 2020 so I added it to The UK Dividend Stocks Portfolio and my personal portfolio.

SThree's valuation is now far less attractive

In the end, SThree's recovery appeared more quickly than I'd expected and the share price has increased by more than 150% in barely 18 months.

This rapid price rise is very welcome, but it does make SThree's shares less attractively valued.

For example, when I bought the shares in early 2020 the potential dividend yield (assuming SThree's dividend would return to its pre-pandemic high of 14.5p) was 6.7%. Today it's 2.5%. You don't have to be a rocket scientist to know that a potential 6.7% yield is better than a potential 2.5% yield, especially if we're talking about exactly the same company.

Rather than just looking at dividend yield, which only takes account of next year's dividend, the theoretically correct way to value companies is to estimate their fair value by estimating their dividends over many years. Having done that, we then need to discount those future dividends because a £10 dividend paid in 2030 is less valuable than a £10 dividend paid tomorrow (just ask yourself which one you'd rather have).

So we need to build a discounted dividend model and in SThree's case, my model is fairly simple. All we need to do is think about the external and internal constraints to growth.

External constraints are things like the size of the market and the company's market share. For example, a company with a 90% market share of a shrinking market obviously has some serious constraints on its future growth.

In SThree's case, it has a very small share (about 1%) of the global STEM recruitment market and that market is expected to grow materially over the next decade and beyond. So there's a lot of room for growth and I don’t think external constraints are going to be a major issue.

Internal constraints mostly relate to the amount of profit the company is able to reinvest into its operations to fund its expansion. You can think of this as being a bit like a savings account. If you have a savings account that pays 10% interest (return on capital of 10%) and you spend half of that and reinvest the other half, the capital in the account will grow by 5%.

Companies are basically the same. They produce a return on their capital, some of which is paid out to shareholders and some of which is reinvested for growth.

In SThree's case, I don't think the pandemic has fundamentally changed anything relating to its business, so my assumption is that SThree will continue to generate historically average returns on capital and that it will pay dividends with a historically average level of dividend cover.

Here’s the full dividend model followed by a brief explanation:

If you'd like to have a go at building your own dividend models, you can use my free investment spreadsheet.

The model effectively says that:

- SThree starts 2021 with 121p of capital per share

- It produces a 25% return on capital in 2021, which is above the historic norm because of pent-up demand created during the pandemic

- The dividend in 2021 is relatively small as management are still being cautious

- Capital employed in 2022 is 141p thanks to 20p of earnings retained in 2021

- In 2022, SThree produces a historically average 17% return on capital, generating earnings of 24p

- Dividend cover in 2022 returns to a historically normal 1.6, returning the dividend to pre-pandemic levels

- From 2023 onwards, return on capital and dividend cover remain broadly the same, which means SThree retains enough earnings to grow at 8% per year

- Beyond 2030, SThree can maintain growth at 4.5% per year

Obviously, this model will turn out to be wrong because the future is unknowable. However, that's not the point. The point is that a dividend model should be realistic and conservative, and I think this model is both realistic and conservative.

If we add all those future dividends up and discount them by 7% per year (because a bird in the hand is worth two in the bush) then we get a present value - or fair value - for SThree of £6.75. In other words, according to this model, if we paid £6.75 for SThree we would receive an annualised return of 7% over the company's remaining lifetime, which matches the expected return of the overall UK stock market (hence the name, fair value).

If instead we add all those future dividends up and discount them by 10% per year then we get a present value - or good value - for SThree of £3.03. In other words, according to this model, if we paid £3.03 for SThree we would receive an annualised return of 10% over the company's remaining lifetime. I call this "good value" because 10% is my target rate of return.

SThree's fair value of £6.75 is comfortably above the current share price of £5.84, so according to this model, SThree is still trading below fair value.

So why am I selling if the shares are still "undervalued"?

There are two reasons:

- The model portfolio has too many holdings (28) and I'm looking to reduce that down to something in the 20 to 25 range. This will allow me to focus the portfolio on its best holdings.

- At £5.84, SThree's share price only has a margin of safety of 24% (margin of safety tells you where the current price is between good and fair value). Some of the portfolio's holdings have a margin of safety of more than 100%, so it makes sense to sell SThree and reinvest the proceeds into those more attractive (and much higher yield) holdings.

So that's exactly what I've done.

I sold SThree a few days ago and reinvested most of the proceeds into a high yield FTSE 100 company with an estimated margin of safety comfortably above 100% and a target position size of around 5%.

* At the time of writing I own shares in Next and Next is a holding in the UK Dividend Stocks Portfolio.

No time for spreadsheets or annual reports?

If you like this article but don’t have hours each month to dig through company accounts, you might find my monthly investment newsletter useful.

Once a month I send out a plain‑English PDF showing:

- The full UK dividend stocks model portfolio

- Which shares I’m buying, selling, trimming or topping up

- The latest news and trading updates for each holding

- Where we are in the stock market valuation cycle

All designed so a UK investor can stay on top of their dividend portfolio in well under an hour a month.

Get the latest blog posts & a free checklist

Get my latest articles in (at most) one email per week and download my dividend investing checklist. Topics usually include:

- Detailed reviews of high-quality UK dividend stocks

- Updates on my UK dividend stocks portfolio

- FTSE 100 and FTSE 250 valuations

- "How to" articles covering all aspects of dividend investing

No spam. Unsubscribe anytime.