In 2018, the global economy went through what is technically known as “a wobble”, causing my portfolio’s most fragile holdings to teeter-totter and, in some cases, shatter. The resulting post-sale reviews of The Restaurant Group, Ted Baker and Xaar contain many painful lessons.

The main lesson was that quality matters, so I set about updating my investment checklist and the UK Dividend Stocks portfolio to focus on quality first and valuation second.

That led to a slew of purchases in 2020, with eight high-quality dividend stocks joining the portfolio. Schroders was the second.

At the end of May, after six broadly satisfactory years, I decided to sell Schroders. Not because its quality has diminished (it hasn’t), but because the valuation is no longer attractive and, more importantly, because Schroders is (sadly) due to be acquired later this year.

The rest of this review is taken more or less directly from the June issue of my monthly newsletter. If you're interested, you can download the original PDF version of this review below:

My buy and sell reviews follow the same 25-step process from my investment checklist, which asks the following five high-level questions:

- Will the portfolio still be broadly diversified after buying/selling this company?

- Does the company have a robust financial track record?

- Does the company have a high-quality core business?

- Does it have good long-term growth prospects?

- Is the share price attractive?

Hopefully, having read through this pre-sale checklist, you’ll have a better idea of what to look for in a quality dividend stock, and a clearer idea of what a disciplined sell process looks like.

1. Will the portfolio still be broadly diversified by company?

YES: Having a sufficiently diversified portfolio is critical when you're investing in individual companies rather than funds.

In this case, when Schroders leaves my portfolio, the number of holdings will fall to 21. That’s far less than my old pre-pandemic target of 30 holdings, but it’s still slightly above the 19–20 range I’m aiming for now that the portfolio is focused on higher‑quality companies.

2. Will the portfolio be broadly diversified by sector?

YES: Although the portfolio already meets my diversification rule of having no more than two holdings from any one sector, I do think (somewhat counterintuitively) that selling Schroders will make the portfolio more diverse, not less. That’s because the portfolio is currently quite heavily weighted towards financial stocks. In fact, the five largest holdings (Admiral, IG, Chesnara, Schroders, Legal & General) all operate in one financial sector or another, and together they make up almost a third of the portfolio, which is a lot.

Although this isn’t necessarily a problem, I would like to reduce the portfolio’s exposure to the financial industry, and selling Schroders is an easy way to move in that direction.

3. Will the portfolio be broadly diversified by country?

YES: Schroders generates around 60% of its revenues from overseas, which is about the same proportion as the overall portfolio. This means removing Schroders will have very little impact on the portfolio’s current UK exposure, with UK revenues likely to stay at around 41%.

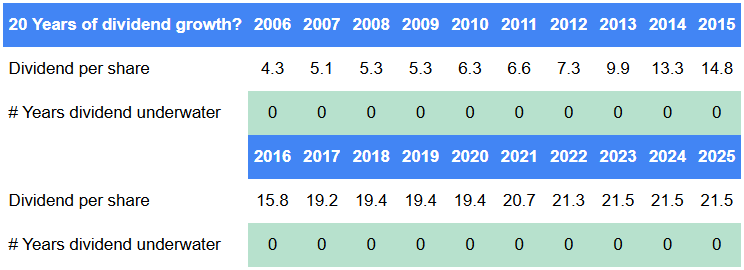

4. Does Schroders have a long track record of progressive dividend growth?

YES: As a general rule, I'm looking for Dividend Hero stocks. These are the elite dividend payers who have managed to avoid any dividend cuts for at least 20 years.

Schroders has achieved that dividend hero status, having held or increased its dividend every single year, giving it a perfect Dividend Underwater score of 0 in 20 years (meaning the dividend never fell below a previous max). The only way to improve that record would be to increase the dividend every year, and very few companies can manage that feat over multiple decades.

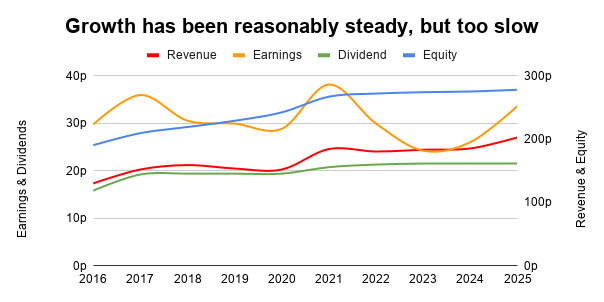

5. Has its growth over the last ten years been good, okay or bad?

BAD: With a Growth Rate of 2.8%, Schroders just fails to meet my minimum ten‑year growth‑rate target of 3%. This isn’t the end of the world, but it does reflect the significant headwinds faced by the business in recent years. Those headwinds mostly came from the rise of low‑ or zero‑cost passive investing, which has proven to be a ferocious source of competition for active investment managers like Schroders.

Those headwinds also negatively impacted its Growth Quality, as Schroders only managed to increase its equity, revenues and dividends 64% of the time over the last ten years, which is below the 67% required for an Okay score and nowhere near the 75% required for a Good score.

Schroders has, of course, responded to the threat of passive investing, and I’ll have more to say about that response when I delve into the company’s strategy.

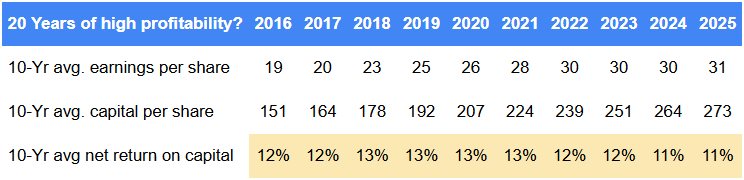

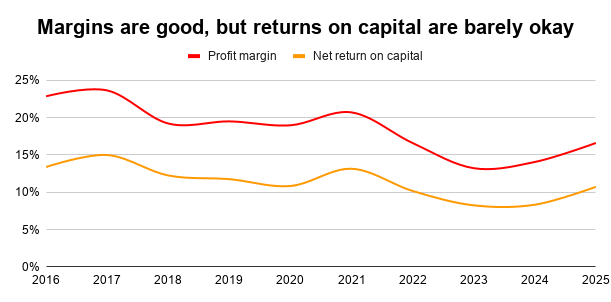

6. Has its profitability been good, okay or bad?

OKAY: When it comes to profitability, Schroders’ track record is comfortably above average in terms of strength and consistency, with a Net ROC score (the ten‑year average net return on capital) of more than 10% (which is the Okay cut‑off point) throughout the last ten years. However, in recent years the previously mentioned headwinds and the pandemic have reduced Net ROC to barely above 10%, so the margin of acceptability has become very thin.

The picture for profit margins is more positive, with the ten‑year average coming in at 18%, which is Good (above 15%).

Being a conservative sort of chap, I’ve given this overall performance an Okay rating, which mildly hints that Schroders may have profit-enhancing competitive advantages.

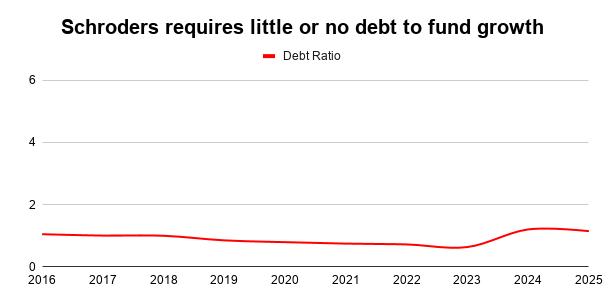

7. Has its balance sheet strength been good, okay or bad?

GOOD: As an investment manager, Schroders doesn’t need to buy expensive factories or machinery in order to grow, so it doesn’t need to borrow large amounts of money to fund such purchases. Instead, it maintains a relatively clean balance sheet, with only a small amount of debt coming from property leases and from £250 million of subordinated debt.

Schroders; total debts of £574 million are barely more than an average year’s earnings, giving the company a very low Debt Ratio of just 1.2.

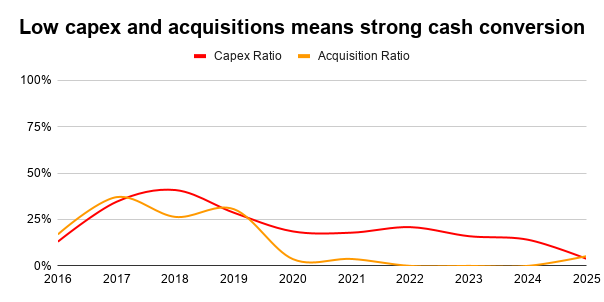

8. Has cash conversion been good, okay or bad?

GOOD: Schroders’ investment management business has little need for expensive factories or machinery, so it has little need for significant capital expenditures. That’s good because capex reduces cash flows without reducing reported earnings, which is why heavy‑capex companies can end up with unsustainable dividends even when their dividend cover is 2× or more. In Schroders’ case, its Capex Ratio (the ratio of ten‑year total capex to ten‑year total earnings) is very low at just 21%.

Acquisitions are another expense that can reduce cash flows without reducing earnings, and here again Schroders has behaved itself. Over the last ten years, the amount of cash spent on acquisitions was only a small fraction of its overall earnings, giving it an Acquisition Ratio (the ratio of ten‑year total cash acquisitions to ten‑year total earnings) of just 12%.

Taken together, this means Schroders’ dividend cover should be a reasonably reliable measure of dividend sustainability; and with dividend cover currently at 1.6, that’s good to know.

9. Has the scale of acquisitions been good, okay or bad?

GOOD: I covered acquisitions in the previous question, but here I’m looking at the whole acquisition picture by including acquisitions paid for with shares rather than cash. Although acquisitions funded by shares don’t directly put the dividend at risk, they can destabilise the core business if they’re too large, so they’re worth investigating.

In this case, Schroders didn’t make any share‑funded acquisitions, which is another sign that this business has a relatively conservative management culture.

10. Does it have a focused core business?

YES: My rule of thumb is that a company should generate at least two‑thirds of its revenue (and preferably profit) from a single, narrowly focused area of activity. Like most large companies, Schroders has several divisions, sub‑divisions and subsidiaries, but at the top level its business is split into Asset Management and Wealth Management.

Asset Management (74% of revenues)

In 2025, this division generated 74% of Schroders’ revenue and 79% of its adjusted operating profit, so this is clearly the core business. The asset management business invests in both public and private assets (those listed on a public exchange and those that are not), and those activities are neatly contained within the Public Markets and Schroders Capital business units.

The Public Markets business actively manages the kind of unit trusts, ETFs and investment trusts we’re all familiar with. These can be invested in by individuals or institutions, and if you’re an institution then Schroders is happy to provide additional services, including the creation of bespoke solutions and funds. Unsurprisingly, this part of Schroders has been hit hardest by the rise of passive investment funds.

Schroders Capital manages private investments, including private equity, private debt, real estate and infrastructure. This makes up about 10% of Schroders’ £824 billion of assets under management (AUM), so it is definitely the smaller part of the asset management business. But it’s also growing fast, and that will be important for the future, as I’ll discuss shortly.

Last but not least, Asset Management is also home to Schroders’ associates and joint‑ventures businesses, which have £94 billion of AUM. This is where Schroders partners with other leading firms in China, Singapore, India and elsewhere to gain a foothold in high‑potential markets.

Wealth Management (26% of revenue)

This division houses two different types of business. On the one hand, Cazenove Capital provides financial advice and wealth management for high and ultra‑high‑net‑worth individuals, families and charities in the UK, while Schroders Wealth Management does the same for international clients. On the other hand, Benchmark Capital provides a technology platform to help financial advisers run their businesses.

Although there are some similarities between asset management and wealth management, they’re different enough that it isn’t entirely obvious why Schroders should bother owning wealth management businesses. That applies even more so to Benchmark, as a tech platform for financial advisers seems to have almost nothing to do with asset management — unless it’s primarily used as a tool to get those advisers to invest their clients’ assets in Schroders’ funds.

In fact, the main purpose of the wealth management division is to allow Schroders to get closer to the ultimate beneficiaries of its investment funds. Getting close to the end customer is a strategy I’m in favour of, as it helps manufacturers (in this case, a manufacturer of investment funds) strengthen their brands with key demographics and improve innovation and product‑market fit, as the company gets information on what customers want directly from the horse’s mouth.

11. Has it had the same core business for at least 20 years?

YES: As you would expect from any company with a history that spans multiple centuries, Schroders has a long and varied past.

The firm was founded in London at the beginning of the 19th century by members of the already prominent Schröder family. Their wealth enabled them to set up new merchant businesses outside their Hamburg base, and membership of Lloyd’s enabled them to insure ships and cargo. Their operations soon expanded into merchant banking, bond issuance and venture capital, and gradually the finance‑focused Schroders of today began to take shape.

In 1924, Schroders launched its first investment trust and in 1926 it started managing client assets, so in terms of Schroders’ current business model, that is where the story begins. But the core business was still investment banking and that remained the case until 2000, when Schroders sold its banking business, turning the remaining firm into a pure‑play investment manager.

Based on that abbreviated history, Schroders has been operating its core asset management business for the thick end of 100 years, and that clearly exceeds my 20-year minimum.

However, it is worth noting that some parts of Schroders were acquired within the last 20 years. This includes most of Schroders Capital, but as that business only makes up a small part of the asset management division, I don’t see this as a major problem. Also, Cazenove Capital was initially acquired in 2013, so that part of Schroders barely passes my 20-year test. Again, that isn’t ideal, but wealth management isn’t the core business, so I also don’t see this as a major problem.

12. Has it had broadly the same growth strategy for at least 10 years?

YES: In 2015, Schroders’ growth strategy had two main pillars: (1) build closer, longer‑term relationships with customers, and (2) actively manage more funds with above‑average performance. These two pillars remain in place today.

Schroders builds closer, longer‑term relationships with institutional clients by working with them to understand their needs and by offering bespoke solutions, portfolios and funds. It does the same for intermediaries, and in the case of financial advisers it does this by supporting their businesses with Benchmark Capital’s platform. And it does the same for individuals and families through Cazenove Capital and Schroders Wealth Management.

Closer, longer‑term customer relationships are useful because they reduce customer churn, which boosts growth as you don’t have to spend as much time and money replacing lost customers. As for managing outperforming funds, this is of course an evergreen requirement for active investment managers.

By 2020, these twin pillars had been joined by a third: rebalancing the business towards private assets and wealth management, where the rise of passive investing was less of a threat. To achieve this, Schroders acquired a series of private‑asset investment firms and wealth managers.

However, the pace of change has been slower than many had hoped, so when a new CEO arrived in 2024, the shift towards private assets and wealth management became more aggressive — and perhaps that’s why the company recently attracted a very reasonable takeover offer.

But, relevant to the question at hand, although the strategy has evolved over the last ten years, with an increasingly urgent emphasis on moving away from public‑market investments, I still think Schroders has pursued broadly the same growth strategy throughout that period.

Fundamentally, the core growth strategy is still to build closer, longer‑term relationships with clients and to actively manage outperforming funds. That foundation remains the same whether clients are invested in public equity funds or private equity funds.

13. Is it free from significant stakeholder risk?

YES: Although Schroders is an investment manager, it isn’t dominated by a single “star” fund manager who could leave and take a big chunk of the firm’s AUM with them, and no single client generates more than 10% of its revenues or profits. On that basis, I don’t think Schroders has an unusually high level of stakeholder risk.

14. Does it gain a durable advantage from market dominance?

NO: My rule of thumb is that to gain a durable advantage from scale alone, a company should be at least twice as large as its nearest competitor.

In Schroders’ case, it is definitely a large company. It’s in the FTSE 100 and has more than £800 billion of assets under management. But that isn’t enough to make it the world’s, Europe’s or even the UK’s largest investment manager. Legal & General, for example, has over £1 trillion of assets under management, so Schroders’ considerable size is not a competitive advantage.

15. Does it gain a durable advantage from hard-to-copy assets?

MAYBE: Most investors know the Schroders brand, and I’m sure almost everyone working in the financial industry knows the name. That certainly helps, but brand awareness isn’t enough. What matters more is the company’s multi‑century history as a trusted supplier of critical financial products and services.

The depth and robustness of that reputation matter. Pension funds and other institutional clients want overwhelming evidence of competence. Perhaps even more importantly, they want an investment manager whose name they can sell to their boss, and who can legitimately take the blame if things go wrong.

In other words, the old “nobody ever got fired for hiring IBM” saying applies in spades, and I doubt any pension fund trustee ever got fired for hiring Schroders.

This reputational advantage is also durable because younger competitors can’t innovate their way to a 200‑year history. You have to earn it one year at a time, and most companies never get close.

Having said all that, while I do think the Schroders brand and history are a durable competitive advantage, I don’t think they give the company an enormous amount of pricing power. Institutional clients have teams of people doing contractual due diligence, so Schroders can’t simply raise prices by 10% and hope nobody notices. This is very different from a loved consumer brand like Vimto (produced by Nichols, which is also in the portfolio), where a 10% price rise adds 20p to a £2 can of soda — something many people would barely notice.

On that basis, I do think the Schroders brand is a durable advantage, but only a weak one.

16. Does it gain a durable advantage from its business model?

NO: Schroders is primarily a manager of public and private assets, with smaller wealth management and financial adviser platform businesses on the side.

From a wealth manager and financial adviser perspective, this gives Schroders a vertically integrated business model, which is something I’m generally in favour of. In other words, a wealth manager from Schroders (via Cazenove Capital) can manage your wealth, and they might put your money into at least one Schroders fund. Or, an independent financial adviser could help you with your finances, and if their business runs on Benchmark’s platform, they might advise you to put some of your money into a Schroders fund.

Vertical integration gives Schroders more control over the supply chain, from creating and managing funds to supporting financial advisers with their businesses or having its own customer‑facing wealth managers. This can make a business more complex, but it can also improve service quality and reduce value leakage to third‑party suppliers (in other words, you don’t have to pay for someone else’s profit margin if you do most of the work yourself).

This is all very interesting, but it’s far from unique. Aviva, M&G and even Hargreaves Lansdown offer funds and financial advice, so vertical integration in this case is a good idea, but it isn’t a durable competitive advantage.

17. Does it gain a durable advantage from focusing on the long term?

YES: Most companies are overly focused on the short term, which I define as the next five years. Some companies make decisions where the benefits will only arrive in the medium term (five to ten years), but very few think seriously about what will happen beyond the next ten years. That rarity is why a consistent long‑term focus can be a powerful competitive advantage.

There are two fairly reliable ways to identify companies with a consistent long‑term mindset: (1) they grow their own CEOs, spending many years developing their best people into CEO candidates with deep knowledge of how the business and its industry work; (2) the founding family has a controlling or near‑controlling stake, which reduces the influence of institutional shareholders with short‑term agendas.

In Schroders’ case, the founding Schröder family still owns almost half the company, and given that the family has been invested in this business for multiple centuries and multiple generations, their interests are clearly focused on the very long term. This is good because it allows Schroders to escape the 3–5‑year mind‑trap that many companies fall into, where every capital investment or operational adjustment has to deliver a material financial return within that narrow timeframe.

A consistent long‑term mindset has enabled Schroders to expand into high‑potential emerging markets where meaningful returns won’t arrive for at least ten or twenty years. Short‑termist competitors prefer to wait until a market reaches maturity and quick returns appear possible, but by the time they enter, Schroders is already a significant and long‑established player.

18. Does it gain a durable advantage from network effects?

NO: There are no network effects in investment management or wealth management.

19. Does it gain a durable advantage from switching costs?

MAYBE: There are some aspects of Schroders’ business where clients face significant barriers if they want to switch to another supplier.

For example, pension fund clients with complex bespoke portfolios and liability‑driven investment strategies would have to identify, vet and transfer funds to one of Schroders’ competitors, and that takes time (and time is money).

The barriers are perhaps even higher for a wealthy family whose financial affairs have been managed by Cazenove Capital for generations, giving Cazenove’s wealth managers deep insights into the family’s affairs that would be impossible for a competitor to replicate without spending years getting to know them.

Given that 81% of Schroders’ AUM comes from institutional and wealth management clients, this could be a meaningful and durable advantage.

Having said that, switching costs are my least favourite competitive advantage, as it often leads to conflicts of interests with customers, where companies try to lure in unsuspecting customers only to ensnare them with barriers to exit. Instead, I like to invest in companies where customers are loyal because the company provides excellent products and services, not because they've fallen into a trap from which they cannot escape.

20. Is it free from serious short-term problems?

YES: Although Schroders’ progress has been slowed by the relentless rise of low‑cost passive investing, that is a medium‑ to long‑term problem rather than a short‑term one. In terms of short‑term issues, as far as I can tell there are none of any significance.

21. Is the core market likely to grow over the next ten years?

YES: This is an interesting question because Schroders is resolutely an active investment manager operating in a world that has been moving towards passive investing for many years. This shift has been a significant headwind for its mutual fund business, leaving it with essentially no growth over the last ten years. That is precisely why Schroders has shifted its business towards markets where the rise of passive funds is less of an issue.

For example, Schroders Solutions solves complex investment problems for institutional clients, and this business has approximately doubled in size over the last ten years. Wealth management is another area where passive funds are less of an issue, as wealth managers earn their cut even if they put client money into low‑cost passive funds. And the good news is that Schroders’ wealth management AUM is about four-times larger than it was a decade ago.

Schroders has already significantly transitioned away from public-market mutual funds, as the majority of its revenue now comes from institutional solutions, private asset funds and wealth management. Given that these areas are expected to grow at least in line with GDP to 2030 and beyond, I do think Schroders’ core market is likely to grow over the next ten years.

22. Does it have a proven ability to grow into adjacent markets?

YES: Over more than two centuries, Schroders has expanded from its merchant‑banking origins into many new markets, both in terms of products and services (including wealth management and investment management) and in terms of geography (including the US, Europe and Asia).

23. Is the dividend yield good, okay or bad?

OKAY: At 3.7%, Schroders’ dividend yield falls into the Okay 3-5% bracket.

24. Are the PE10 and PD10 ratios good, okay or bad?

OKAY: PE10 and PD10 are the price to 10-year average earnings and dividend ratios respectively. I use these ratios because the standard PE and dividend yield only compare share prices to last year's earnings and dividends, so they can be seriously distorted by unusually good or bad results in a single year.

At 19 and 29, Schroders' PE10 and PD10 ratios are Okay (15-25) and Good (0-30) respectively. As the PD10 ratio is very close to the Good/Okay border, I've given them an Okay rating overall.

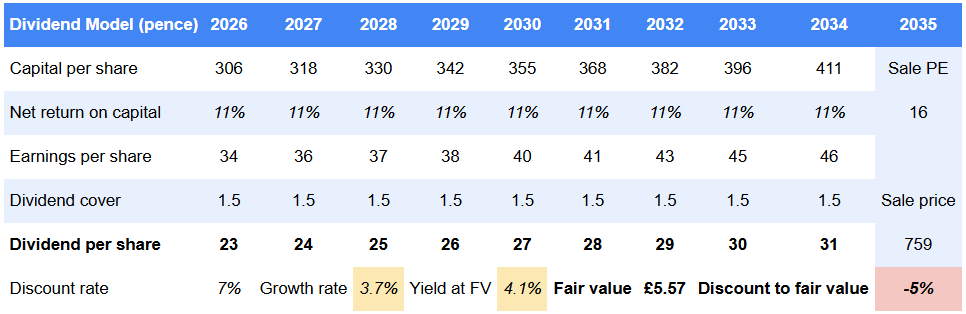

25. Is there a sufficient discount between price and fair value?

NO: Schroders is about to be taken over by US investment manager Nuveen at £5.90 per share. At the end of May the share price was £5.84, which was above my fair value estimate of £5.57.

That fair value estimate is based on the assumption that Schroders continues to generate historically average net returns on capital, keeps dividend cover at a historically average level of 1.5, and is sold after ten years at a historically average PE ratio. Those assumptions produce the following discounted dividend model:

Conclusion: Should I sell this holding?

YES: Schroders does still meet most of my quality criteria, but at today’s price it no longer meets my valuation criteria. That, plus the impending takeover, is why I have decided to sell.

In terms of the final results, it’s somewhat complicated because the investment came in three legs, with each delivering double-digit annualised returns.

The first leg began and ended in 2020, when I purchased SDR shares for £23.45 and sold them just a few months later at £28.59 for an annualised return of 49%.

The second leg began when I then purchased the cheaper SDRC shares in 2020 and 2022 at an average price of £18.51 (the SDRC shares were usually cheaper because they didn't have voting rights). Towards the end of 2022, the SDRC share class was cancelled and converted into SDR (voting) shares. The portfolio’s SDRC shares were effectively sold at an average price of £22.92, which gave this leg of the investment an annualised return of 25.3%.

The last leg began when the SDRC shares were consolidated into SDR shares in 2022. I later topped up the investment, giving the pool of shares an average purchase price of £4.46.

I sold the entire Schroders position at the start of June for £5.83 per share, giving an annual return for the final leg of 13.0%.

Along the way, Schroders also paid a high and reliable dividend, and as I’m a dyed-in-the-wool dividend investor, this is of course an important aspect of the overall investment.

In summary then, this was a good investment, and I think it's sad to see a high quality company like Schroders leaving the UK stock market.

As for the proceeds of this sale, I immediately reinvested some into Telecom Plus, and the rest will be reinvested into new or existing holdings over the next month or so.

Note: Any holdings mentioned in the article were holdings in both the UK Dividend Stocks Portfolio and my real-world portfolio at the time of writing.

No time for spreadsheets or annual reports?

If you like this article but don’t have hours each month to dig through company accounts, you might find my monthly investment newsletter useful.

Once a month I send out a plain‑English PDF showing:

- The full UK dividend stocks model portfolio

- Which shares I’m buying, selling, trimming or topping up

- The latest news and trading updates for each holding

- Where we are in the stock market valuation cycle

All designed so a UK investor can stay on top of their dividend portfolio in well under an hour a month.

Get the latest blog posts & a free checklist

Get my latest articles in (at most) one email per week and download my dividend investing checklist. Topics usually include:

- Detailed reviews of high-quality UK dividend stocks

- Updates on my UK dividend stocks portfolio

- FTSE 100 and FTSE 250 valuations

- "How to" articles covering all aspects of dividend investing

No spam. Unsubscribe anytime.