Investors love to talk about the stock-picking side of investing because, for most of us, that’s the really interesting bit.

However, although portfolio diversification may be a less sexy topic, it is at least as important as choosing the right stocks and, in many ways, it’s more important.

So, having recently refreshed and simplified my diversification rules, I thought this would be a good time to give you a whistle-stop tour of seven simple rules you can use to diversify a defensive dividend portfolio.

Table of contents

- How to diversify a portfolio to reduce three key risks

- How to tilt a portfolio towards lower-risk dividend stocks

How to diversify a portfolio to reduce three key risks

There are three main risks we can reduce through diversification, so let’s take each one in turn.

Diversify to reduce company risk

A snapshot of holdings from the UK Dividend Stocks Portfolio

The most obvious form of diversification is to simply spread your money across a number of different investments.

This leaves us with two questions: First, how much company-specific risk can you tolerate, and second, how much are you going to invest in one company versus another?

How much company-specific risk can you tolerate?

In terms of your risk tolerance, there is a tradeoff.

The more risk you can tolerate, the more you can invest in each company and the fewer stocks you'll need to own. That means you’ll be able to build your portfolio around a handful of the very best stocks, with the highest yields and the highest growth potential, but you’ll also be exposed to larger losses if one of those investments goes seriously wrong.

Before you decide how much to invest in each company, one thing to remember is that most people overestimate their ability to tolerate risk.

They think they’ll be able to handle relatively large positions of around 10% or more, and that’s fine when things are going well, but when events take a turn for the worse and their 10% position shrinks to 5%, their emotions can start to take over the decision-making process.

That’s a problem because as investors, we’re supposed to think rationally and logically, and to do that, we need to have a suitable degree of emotional detachment from our investments.

If an investment begins to make you nervous then you’re unlikely to think rationally about it, and that’s a good sign that your position size is too large. So, I suggest you err on the side of caution.

In my case, I know from experience that I start to feel uncomfortable when a position exceeds 6% of my portfolio, so I use the following rule of thumb:

Rule of thumb: If a position exceeds 6% of the portfolio, trim it back to its target size

6% isn’t a magic number and you may want to set your limit higher or lower than that, but you should still have a rule about trimming oversized positions.

How much are you going to invest in one company versus another?

The rule above mentions the idea of a “target size”. This is effectively the ideal size for a particular investment.

For example, the FTSE 100 is a market cap-weighted index, so the ideal position size for each holding is based on its market capitalisation. In other words, a company worth £2 billion will have a target position size twice that of a company worth £1 billion.

Some indices are yield-weighted, where a stock with a 4% dividend yield will have a position size twice that of a stock with a 2% dividend yield, and other indices are equally weighted, where all holdings have exactly the same target size.

Having used both a simple equal-weight system and a more complex position-sizing system based on each holding’s valuation and defensiveness, I must admit that I prefer the elegant simplicity of an equal-weight portfolio.

One of the main benefits of equally weighted portfolios is that they’re much easier to manage. You just pick a target position size based on your ability to tolerate risk and you’re good to go.

For example, my maximum position size is 6% and when a holding expands beyond that level, I’ll trim it back to target. But what should that target be?

In my case, I’ve set the target size to be 4%, which is far enough below 6% so that rebalancing trades are reasonably large (to reduce the impact of broker fees) and relatively infrequent (because I have better things to do than fiddle about with position sizes).

A 4% target size also means my portfolio will hold around 25 stocks and, from experience, I know that’s enough to keep the portfolio broadly diversified, but not so many that managing the portfolio becomes an annoying chore.

Rule of thumb: All positions have an equally weighted target size of 4%

Diversify to reduce industry risk

Spreading your investments across many different companies will go a long way towards diversifying your portfolio, but if all of those companies operate in the same industry then your portfolio will be less diverse than you think.

Fortunately, industry risk is easy to reduce. All you have to do is set a limit on how many stocks you'll own from one industry or sector.

I use the official ICB sectors for this, which you can find for any UK-listed company on the London Stock Exchange website (under each company's “our story” section) or through other data providers such as SharePad.

My rule for reducing sector-specific risk is very simple:

Rule of thumb: No more than 10% of the portfolio’s holdings can be in the same sector

For example, with 25 holdings, no more than two holdings can operate in the same sector, so that’s two retailers, two life insurers, two banks, and so on. I like to think of it as the Noah’s Ark rule of diversification.

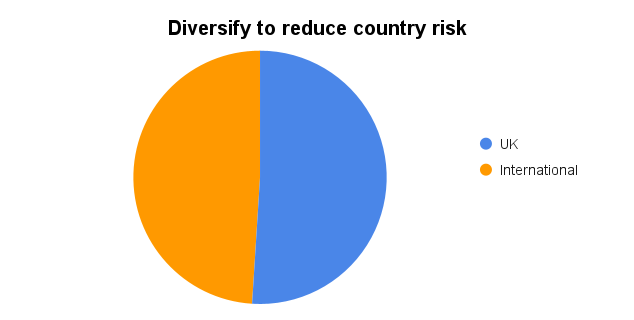

Diversify to reduce country risk

We also need to think about country risk. If we invest in lots of different companies in lots of different industries then that sounds great, but if all of them operate in the same country the portfolio could struggle if that country finds itself in a prolonged depression, war or other disaster.

As with company and industry risk, the easiest way to deal with country risk is to limit the amount you’re willing to invest in a single country. For example, here’s my rule:

Rule of thumb: No more than 50% of the portfolio’s revenues can come from one country

Ideally, I would like to be more geographically diversified than this, but as a UK investor who only invests in FTSE All-Share stocks, finding sufficient numbers of companies that are good quality, good value and largely devoid of UK exposure is harder said than done.

Given that constraint, I think a 50% limit still strikes a reasonable balance between reducing country risk and not making the task of finding a diverse group of good quality, good value stocks too difficult.

If you're not 100% invested in UK stocks then adding more geographic diversity is easily done by investing some of your portfolio into internationally-focused stocks or funds.

How to tilt a portfolio towards lower-risk dividend stocks

At this point, we now have a portfolio that is diversified across many companies, industries and countries, and that’s a good start.

But I’m a defensive dividend investor and this post is about diversifying a defensive dividend portfolio, so there are a few additional rules we can apply to make the portfolio even more defensive.

Tilt the portfolio towards defensive stocks

This one is pretty obvious. If you’re looking to build a defensive dividend portfolio then it may be a good idea to include a reasonable number of holdings from defensive sectors, such as Unilever or British American Tobacco (both of which I currently hold).

As a dividend investor, I define sectors as defensive, cyclical or highly cyclical based on their impact on dividends:

- Quality companies in defensive sectors don’t usually cut their dividend in a recession

- Quality companies in cyclical sectors might cut their dividend in a recession, but they don’t usually suspend it

- Quality companies in highly cyclical sectors might suspend their dividend, but they don’t usually suspend it for multiple years

Here’s a list of all the defensive sectors:

- Beverages

- Electricity

- Food Producers

- Gas, Water and Multi-utilities

- Health Care Providers

- Medical Equipment and Services

- Personal Care, Drug and Grocery Stores

- Pharmaceuticals and Biotechnology

- Renewable Energy

- Telecommunications Service Providers

- Tobacco

When I first started tilting my portfolio towards defensive stocks a few years ago, I used a somewhat elaborate system of position sizing which gave defensive stocks a larger target size.

That approach worked, but I now prefer a simpler approach that achieves more or less the same outcome whilst retaining the elegant simplicity of an equally weighted portfolio. All you have to do is set a lower limit on how many defensive stocks you’ll hold.

Again, there is a trade-off to be made. Defensive stocks are usually lower risk and lower risk investments usually have lower returns. More specifically, defensive stocks will typically have either a lower dividend yield or lower growth prospects, and sometimes they’ll have both.

Personally, I’m trying to balance the upsides of holding defensive stocks (steadier dividends) with the downsides (lower income and/or growth), so my rule isn’t overly demanding:

Rule of thumb: At least 20% of the portfolio’s holdings should be in defensive sectors

For example, a portfolio with 25 holdings would hold at least five defensive stocks, and I think that should be enough to add some meaningful stability to a portfolio's overall dividend, especially during future recessions.

Tilt the portfolio away from highly cyclical stocks

Another way to tilt a portfolio towards the more defensive end of the market is to tilt it away from the more cyclical end. Again, the easy way to do this is to simply hold fewer highly cyclical stocks. Here’s a list of all the sectors I define as highly cyclical:

- Chemicals

- Construction and Materials

- Household Goods and Home Construction

- Industrial Materials

- Industrial Metals and Mining

- Non-Renewable Energy

- Oil, Gas and Coal

- Precious Metals and Mining

I think it would be entirely reasonable to exclude all highly cyclical stocks from a defensive dividend portfolio, but I like to be more accommodating as there are some surprisingly robust companies operating in these sectors.

Even so, highly cyclical stocks are usually higher risk and their dividends are usually quite sensitive to the ups and downs of the economy, so I do limit my exposure to them using the following rule, which mirrors the rule for defensive stocks:

Rule of thumb: No more than 20% of the portfolio’s holdings should be in highly cyclical sectors

Tilt the portfolio towards large companies

The final tilt towards larger companies is another obvious one.

Large companies are generally better suited to defensive dividend portfolios because they tend to be more robust than small companies.

That's because they usually have more experience, deeper relationships with suppliers, customers and employees, and more financial firepower and employee brain-power to pull them out of whatever ditch they may occasionally drive themselves into.

There are all manner of rules you could come up with for this, such as only investing in FTSE 100 stocks or FTSE 350 stocks. Again, those are reasonable, but as with highly cyclical stocks, I prefer to be more accommodating and I’m happy to invest in a few small-caps, but only if their quality and value are good.

Rule of thumb: No more than 20% of the portfolio’s holdings should be small-caps

Conclusion: Diversifying your portfolio doesn’t have to be complicated

So there we have it; seven simple rules for diversifying a defensive dividend portfolio.

These rules (or something similar) will reduce a portfolio’s exposure to any one company, industry or country, and they’ll make sure the portfolio has a healthy tilt towards larger and more defensive companies.

Broad diversification certainly isn’t the holy grail of investing, but it has been called the only free lunch in investing, and for most investors it isn’t just free, it’s essential.

Disclosure: I own shares in Legal & General, Chesnara, MoneySuperMarket, Next, Direct Line, Unilever and British American Tobacco

No time for spreadsheets or annual reports?

If you like this article but don’t have hours each month to dig through company accounts, you might find my monthly investment newsletter useful.

Once a month I send out a plain‑English PDF showing:

- The full UK dividend stocks model portfolio

- Which shares I’m buying, selling, trimming or topping up

- The latest news and trading updates for each holding

- Where we are in the stock market valuation cycle

All designed so a UK investor can stay on top of their dividend portfolio in well under an hour a month.

Get the latest blog posts & a free checklist

Get my latest articles in (at most) one email per week and download my dividend investing checklist. Topics usually include:

- Detailed reviews of high-quality UK dividend stocks

- Updates on my UK dividend stocks portfolio

- FTSE 100 and FTSE 250 valuations

- "How to" articles covering all aspects of dividend investing

No spam. Unsubscribe anytime.